Verein Deutscher Zementwerke e.V. (VDZ), the German cement association, recently released a report outlining the cement and concrete decarbonisation roadmap for Germany to achieve a low-carbon future.

Decarbonising Cement and Concrete: A CO2 Roadmap for the German Cement Industry focuses on the challenges and opportunities for the cement and concrete sectors—and why it will take the collaboration of everyone across the value chain in the construction industry to get to net zero.

Challenges Facing Germany’s Cement and Concrete Industries

Germany is not unique in facing significant obstacles to reaching net zero emissions—and its journey is one that others around the world can learn from.

The cement and concrete industries have long focused on reducing their environmental impact and, since 1990, German producers have reduced CO2 emissions by 20-25%. This can largely be attributed to two actions: the reduction of clinker content in cement and the increased use of alternative fuels instead of the traditionally used fossil fuels.

The country is now at an important juncture. Existing methods to decarbonise cement and concrete are reaching their limits. In order to achieve net zero, more action needs to be taken at all stages of the construction industry’s value chain.

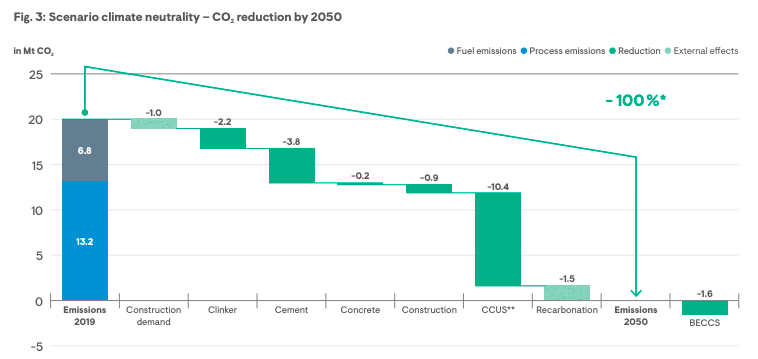

Two Decarbonisation Scenarios

The VDZ roadmap outlines two pathways to the decarbonisation of cement and concrete in Germany by 2050:

- Ambitious reference scenario: This assumes the enhanced deployment of currently available CO2 reduction technologies and is based on very challenging assumptions.

- Climate neutrality scenario: This goes further than the ambitious reference scenario to reach the limits of what is technically feasible today, plus breakthrough technologies.

One of the most exciting of these breakthrough technologies is carbon capture, utilisation, and storage (CCUS). CCUS makes it possible to capture up to 100% of the carbon emissions from cement manufacturing. These can be stored safely underground, injected back into concrete to strengthen it, or used to make other products like synthetic aggregates or fuels.

Analysis of the two scenarios reveals that only the climate neutrality scenario will enable the German cement industry to achieve net zero emissions by 2050.

The Critical Role of CCUS

As the scenarios outline, reaching net zero isn’t possible without breakthrough technologies like CCUS. VDZ projects that “after exhausting all other levers of CO2 mitigation it will be necessary to capture around 10 million tonnes of CO2 annually from the year 2050 onwards.”

To achieve this, the development of new value chains will be necessary to ensure that CO2 is appropriately stored and utilised following its capture.

The creation of these value chains is in process. Svante is a carbon capture technology that takes CO2 directly from industrial sources at less than half the capital cost of other solutions.

CarbonCure introduces recycled CO₂ into fresh concrete to reduce its carbon footprint without compromising performance. The CO₂ is currently captured from industrial emitters like ethanol plants but the company has plans to use direct air capture carbon in the future—and this use case was proven with Svante as part of the Carbon XPRIZE.

Three Requirements for Cement and Concrete Decarbonisation Success

Cement producers cannot reach net zero alone. VDZ emphasises the need for collaboration to drive wider societal, political, and economic changes to make carbon neutrality a reality.

1. Cooperation along the value chain

Globally, building and construction are responsible for 39% of all carbon emissions. While cement is a contributor, change has to involve the entire industry. VDZ calls for “cooperation of the entire value chain, from equipment suppliers and concrete manufacturers through to the building industry, designers and architects.”

2. Effective policy frameworks

Change needs to be mandated from the top. As VDZ describes, this will help to “ensure a level playing field to allow the competitive production of low-carbon and successively decarbonised cements."

For example, new procurement policies in the U.S. have made low-carbon concrete a viable option in places including Portland, Marin County, Hawaii, Austin, and New York State. CarbonCure’s policy page keeps a running tally on these legislative changes.

3. Promotion of “green” products

Finally, everyone in the building industry has a role to play in promoting the market for “green” products. VDZ highlights that these “tend to be considerably more expensive than those produced conventionally” but the industry can capitalise on a global shift toward sustainability—accelerated by the COVID-19 pandemic—to increase the supply of green products to a market increasingly motivated to choose them.

Want to learn more? Read our ebook, CarbonCure’s Path to the Decarbonization of Concrete or watch our webinar with the Cement Association of Canada and Lafarge Canada.

CO₂ Mineralization in Concrete: A Proven Path to Lower Carbon Without Compromising Performance

Fly Ash and Innovation in Concrete